What happens when the bills keep coming, collection calls become routine, and every paycheck seems gone before it arrives? For many Texans, financial pressure builds slowly until it becomes impossible to ignore. Medical expenses, credit card balances, personal loans, business setbacks, or sudden income loss can place families in a position where basic monthly obligations become difficult to manage.

Hundreds of thousands of bankruptcy cases are filed across the country every year. Many of those filings involve people who delayed getting information because they feared losing everything or believed bankruptcy meant failure.

Understanding legal rights before taking action can make a major difference. Filing bankruptcy is not simply about eliminating debt. It is also about protecting property, stopping collection activity, understanding court obligations, and choosing the right form of relief under federal law.

This article explains what individuals should know before they file for bankruptcy relief in Texas, including legal protections, property exemptions, repayment options, common mistakes, and how a bankruptcy lawyer may help people make informed decisions.

Why Understanding Your Rights Matters Before Filing

Bankruptcy law gives consumers legal protections, but many people enter the process without fully understanding what those protections include. Some wait too long and drain retirement accounts. Others transfer property, repay relatives first, or continue using credit cards in ways that later create legal problems.

Learning about bankruptcy rights before filing may help individuals:

- Protect exempt property

- Stop collection lawsuits and creditor harassment

- Understand repayment responsibilities

- Avoid filing errors

- Determine whether Chapter 7or Chapter 13 is more appropriate

- Reduce stress caused by uncertainty

Federal bankruptcy laws exist to give qualified individuals a chance to regain stability. However, those protections work best when people understand how the process functions before filing paperwork.

The Right to Seek Bankruptcy Protection

One of the most important rights consumers have is the legal right to seek bankruptcy relief. Creditors cannot prevent a qualified person from filing simply because money is owed.

Bankruptcy protection is available to individuals facing many types of financial hardship, including:

- Credit card debt

- Medical debt

- Personal loans

- Certain lawsuit judgments

- Repossession threats

- Foreclosure proceedings

- Utility shutoff concerns

- Business-related personal debt

People often hesitate because they fear social judgment. However, bankruptcy laws exist because Congress recognized that financial setbacks can happen to anyone.

A bankruptcy attorney in Corpus Christi may explain how federal protections apply to a person’s specific situation and whether filing may provide relief.

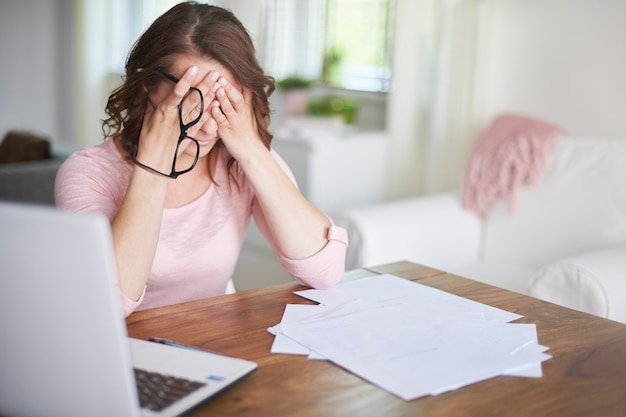

Understanding the Automatic Stay

Image Filename: distressed-woman-financial-struggles

Image Alt Text: A woman sitting in distress with papers scattered on the table and a laptop open beside her, overwhelmed by financial difficulties.

Image Caption: Financial stress can be overwhelming—this woman struggles with paperwork and tough financial decisions.

When a bankruptcy case is filed, the court issues something called an automatic stay. This legal protection temporarily stops many collection efforts immediately.

The automatic stay may stop:

- Collection calls

- Lawsuits

- Bank levies

- Foreclosure actions

- Repossession attempts

- Debt collection letters

- Certain utility disconnections

For many people, this is the first moment of financial relief they have experienced in months or years.

However, there are limits. Some obligations are not affected by bankruptcy proceedings, and repeated filings may reduce the length or effectiveness of the stay. Understanding these limits before filing helps prevent confusion later.

A bankruptcy lawyer in Corpus Christi may explain how the automatic stay applies to pending lawsuits, foreclosure notices, or aggressive collection efforts.

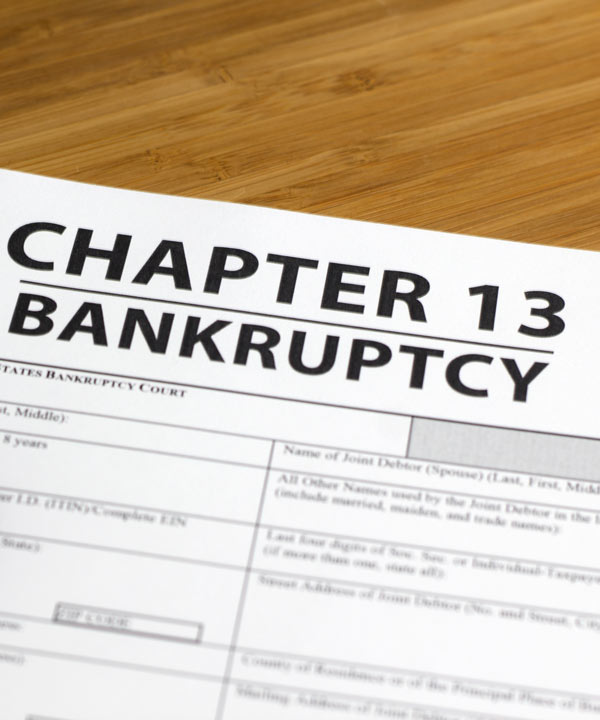

The Right to Choose Between Chapter 7 and Chapter 13

Image File Name: filing-for-bankruptcy

Image Alt Text: A form to file for Chapter 13 bankruptcy

Image Caption: Filing for bankruptcy can feel like a lifeline when debts become unmanageable

Consumers generally have the right to file under different bankruptcy chapters depending on eligibility and financial circumstances.

The two most common forms of consumer bankruptcy are Chapter 7 and Chapter 13.

Chapter 7 Bankruptcy

Chapter 7 is sometimes called liquidation bankruptcy. It is designed for individuals who cannot realistically repay their debts.

In many Chapter 7 cases:

- Credit card debt may be discharged

- Medical debt may be discharged

- Personal loan obligations may be eliminated

- Collection efforts stop during the case

A Chapter 7 bankruptcy attorney may evaluate income, assets, and expenses to determine eligibility.

People often fear they will lose all their belongings in Chapter 7. In reality, Texas exemption laws are among the strongest in the country, and many filers keep most or all of their property.

Chapter 13 Bankruptcy

Chapter 13 involves a structured repayment plan approved by the bankruptcy court. Instead of immediate discharge through liquidation, the filer makes monthly payments over several years.

Chapter 13 may help individuals:

- Catch up on mortgage arrears

- Prevent foreclosure

- Repay certain tax obligations

- Protect nonexempt property

- Consolidate debt payments

A Chapter 13 bankruptcy attorney may explain whether a repayment plan is realistic based on income and expenses.

Choosing between these chapters depends on many factors, including income level, property ownership, debt type, and long-term financial goals.

The Right to Protect Certain Property

One of the biggest misconceptions about bankruptcy is the belief that filing automatically means losing a home, vehicle, or personal belongings.

Texas law provides strong exemption protections for many assets.

Common Exempt Property in Texas

Depending on the circumstances, exemptions may protect:

- Primary residence

- Household furnishings

- Clothing

- Retirement accounts

- Certain vehicles

- Tools used for work

- Some insurance benefits

- Personal items within legal limits

Exemptions determine what property creditors and trustees may or may not take during bankruptcy proceedings.

Proper planning matters because exemption errors can create unnecessary problems. Waiting too long or transferring assets before filing can also create legal complications.

Many bankruptcy lawyers in Corpus Christi, TX review assets carefully before filing to identify available protections under state and federal law.

The Right to Accurate Financial Disclosure

Bankruptcy filers have the right to seek relief, but they also have legal responsibilities. One of the most important is the obligation to provide accurate financial information.

Bankruptcy paperwork requires disclosure of:

- Income

- Expenses

- Assets

- Debts

- Property transfers

- Bank accounts

- Tax information

Honesty is required throughout the process. Attempting to hide property or omit information can lead to serious consequences.

Common Mistakes People Make Before Filing

Some consumers unintentionally create problems because they do not understand the rules beforehand.

Examples include:

- Transferring property to relatives

- Selling assets below market value

- Taking large cash advances

- Using credit cards heavily before filing

- Ignoring court notices

- Withdrawing retirement funds unnecessarily

Understanding these issues before filing may help individuals avoid allegations of fraud or bad faith.

A bankruptcy attorney in Corpus Christi may review recent financial activity to identify concerns before documents are submitted to the court.

The Right to Be Treated Fairly by Creditors

Debt collectors and creditors must follow certain laws even before bankruptcy is filed.

Consumers still have rights under state and federal law regarding:

- Harassing phone calls

- Misleading collection tactics

- False threats

- Improper communication practices

Filing bankruptcy strengthens those protections through the automatic stay, but creditor misconduct may still occur.

If collection efforts continue after filing, the bankruptcy court may impose penalties against creditors who violate the law.

People considering bankruptcy should keep records of collection notices, lawsuits, payment demands, and creditor communication because this information may become important later.

Understanding the Means Test

Eligibility for Chapter 7 often depends on something called the means test.

The means test compares:

- Household income

- Family size

- Allowable expenses

- State median income figures

Its purpose is to determine whether an individual has enough disposable income to repay debts through Chapter 13 instead of Chapter 7.

Passing the means test does not always mean someone has no income. It simply means they qualify under federal guidelines.

This calculation can become complicated for people with:

- Irregular income

- Self-employment earnings

- Recent job changes

- Business expenses

- Multiple income sources

A Chapter 7 bankruptcy attorney may help review whether a person qualifies before paperwork is filed.

Rights Related to Secured Debts

Secured debts involve property used as collateral, such as homes or vehicles.

Bankruptcy may provide several options regarding secured property.

Possible Options Include:

- Continuing payments and keeping the property

- Surrendering the property

- Reaffirming certain debts

- Restructuring payments in Chapter 13

Every option has long-term consequences. For example, reaffirming debt may keep a person legally responsible even after bankruptcy closes.

People should fully understand the legal and financial effects before agreeing to reaffirm secured debt obligations.

A bankruptcy lawyer may explain how different choices affect future obligations and property rights.

Understanding Nondischargeable Debts

Not all debts disappear through bankruptcy.

Some obligations may survive the bankruptcy process depending on the circumstances.

Examples may include:

- Certain tax debts

- Child support obligations

- Alimony

- Some student loans

- Debts involving fraud allegations

- Certain court penalties

People sometimes assume bankruptcy erases every financial obligation, but the law contains important exceptions.

Understanding which debts may remain after filing helps individuals make realistic plans moving forward.

The Right to Legal Representation

Individuals have the right to represent themselves in bankruptcy court, but bankruptcy law contains detailed procedures, deadlines, and documentation requirements.

Mistakes can lead to:

- Case dismissal

- Loss of property protections

- Delayed discharge

- Court sanctions

- Creditor objections

Working with a bankruptcy lawyer may help people understand filing requirements and avoid preventable issues.

Many bankruptcy lawyers in Corpus Christi, TX assist clients with:

- Preparing bankruptcy petitions

- Reviewing exemptions

- Evaluating debt types

- Responding to trustee requests

- Preparing for creditor meetings

- Explaining repayment obligations

Legal guidance may also help individuals determine whether bankruptcy is the right solution at all.

Understanding the Meeting of Creditors

After filing, most bankruptcy cases include a meeting commonly called the 341 meeting or meeting of creditors.

During this meeting:

- A trustee reviews the case

- The filer answers questions under oath

- Creditors may appear and ask questions

In many consumer cases, creditors do not attend. Still, the meeting is an official legal proceeding and should be taken seriously.

Questions often focus on:

- Income

- Assets

- Property ownership

- Debts

- Financial disclosures

Preparing in advance may help the process move more smoothly.

Bankruptcy and Credit Reporting Rights

Many consumers fear bankruptcy will permanently destroy their credit standing. While bankruptcy does affect credit reports, the impact is often more complex than people expect.

For some individuals, continued missed payments and collection accounts may already have caused major credit damage before filing.

Bankruptcy may provide an opportunity to begin rebuilding once debts are discharged.

Consumers also have rights regarding credit reporting accuracy.

After discharge:

- Discharged debts should reflect proper reporting status

- Duplicate collection reporting may be disputed

- Incorrect balances may be challenged

Reviewing credit reports after bankruptcy may help individuals identify reporting errors.

Rights Concerning Foreclosure and Repossession

People facing foreclosure or vehicle repossession often believe they have no remaining options.

In some cases, bankruptcy may temporarily stop these actions through the automatic stay.

Chapter 13, in particular, may provide time to:

- Catch up on mortgage arrears

- Repay missed vehicle payments

- Organize overdue obligations into one plan

However, timing matters. Waiting too long can reduce available options.

Understanding rights early may help individuals make informed decisions before foreclosure sales or repossession actions move forward.

Questions People Should Ask Before Filing

Questions to Consider

- What debts can actually be discharged?

- Is Chapter 7 or Chapter 13more appropriate?

- What property is protected under Texas exemptions?

- Are there pending lawsuits or foreclosure proceedings?

- Has any property been transferred recently?

- Are all tax returns filed?

- Is the current income stable enough for Chapter 13?

- What long-term obligations will remain after bankruptcy?

Gathering this information beforehand may help avoid surprises during the process.

Is Waiting Too Long Making the Situation Worse?

Many people spend years trying to manage debt before speaking with a bankruptcy lawyer. During that time, balances may increase, lawsuits may proceed, and savings may disappear trying to keep up with minimum payments.

Understanding bankruptcy rights before taking action can help people make informed decisions about their legal options. Whether someone may qualify for Chapter 7 or needs a repayment plan under Chapter 13, getting accurate information matters.

The Law Office of Joel Gonzalez assists individuals seeking to file for bankruptcy relief in Texas by helping them understand available protections, court procedures, and debt relief options under federal law.

People searching for bankruptcy lawyers in Corpus Christi, TX, a Chapter 13 bankruptcy attorney, or a Chapter 7 bankruptcy attorney may benefit from speaking with a bankruptcy attorney in Corpus Christi who can review their financial circumstances and explain possible next steps.