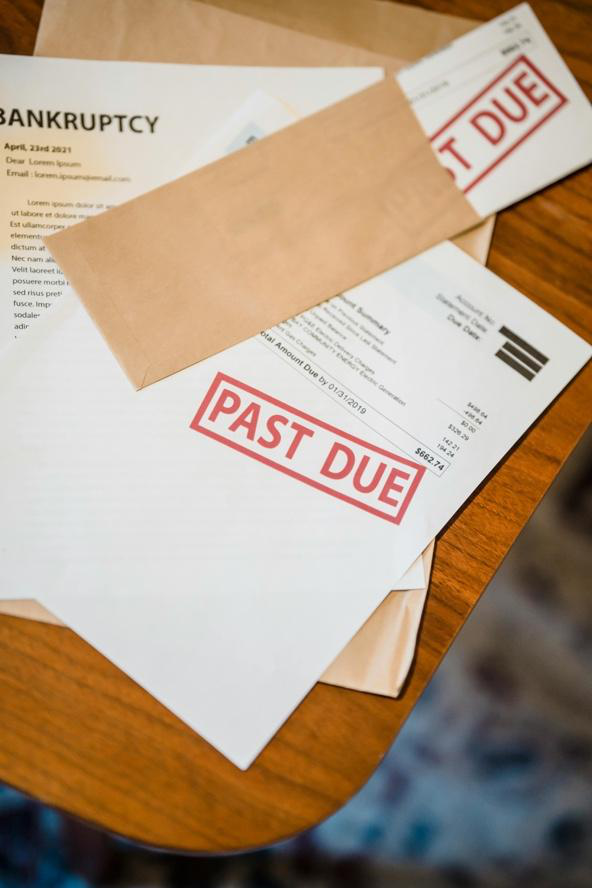

Debt can build gradually or all at once. Medical bills, credit card balances, lawsuits, foreclosure threats, or tax issues can quickly create financial pressure that feels impossible to manage alone. When that happens, understanding your legal and financial options becomes critical.

Debt relief services are not one-size-fits-all. Some solutions focus on negotiating balances. Others restructure payments. In more serious situations, bankruptcy may be a better approach if other options are not realistic. The key is knowing what each service actually does, and what it does not do, before making a decision.

Before choosing a strategy, it is important to understand how each type of debt relief works under Texas law.

What Is Debt Relief?

Debt relief refers to legal or structured financial solutions designed to reduce, reorganize, or eliminate debt when repayment has become unmanageable. It can involve negotiating lower balances, setting up structured payment plans, defending against lawsuits, or, in more serious situations, filing for bankruptcy protection. The goal is not simply to delay payments, but to create a realistic and lawful path toward financial stability.

It is important to distinguish between informal financial help and formal legal debt relief. Informal options might include borrowing from family, temporarily deferring payments, or working out private arrangements with creditors. Legal debt relief, on the other hand, involves structured protections under state or federal law. This may include negotiated settlements, formal dispute responses to lawsuits, or bankruptcy filings that trigger court-supervised protections.

Common debt problems that lead individuals to seek relief include mounting credit card balances, overwhelming medical bills, collection lawsuits, tax levies, and mortgage arrears that place a home at risk. Each type of debt carries different consequences and legal remedies.

Understanding your legal position in Texas is essential before choosing a strategy. A qualified attorney providing debt relief service guidance can evaluate your specific financial situation and determine whether negotiation, structured repayment, or bankruptcy may be the most appropriate solution under Texas law.

Common Types of Debt Relief Services in Texas

Debt Settlement

Debt settlement is a negotiated agreement between a debtor and a creditor to resolve a debt for less than the full amount owed. Instead of continuing minimum payments with accumulating interest, the creditor agrees to accept a reduced payoff as satisfaction of the balance. Settlement is most commonly used for unsecured debts such as credit cards, personal loans, and certain medical bills.

The process typically begins with a financial review to determine hardship. Creditors are more likely to consider settlement when payments have fallen behind or when there is a demonstrated inability to pay the full balance. Once negotiations begin, the creditor may agree to accept either a lump-sum payment or a structured settlement.

A lump-sum settlement involves paying a reduced amount in one payment. Creditors often prefer this option because it resolves the account immediately. A structured settlement, by contrast, allows payments over a short, defined period, often a few months. While structured plans may be easier for some individuals, they require strict compliance with agreed deadlines.

Debt settlement has advantages. It can significantly reduce total balances, stop collection calls once resolved, and avoid bankruptcy in certain cases. However, there are risks. Missed payments during negotiation can harm credit; creditors are not required to settle, and forgiven debt may carry potential tax consequences. In addition, if a lawsuit has already been filed, the settlement must be handled carefully to avoid default judgments.

Settlement is most realistic when the debtor has access to funds for negotiation and when the total debt load is manageable. If income is stable and the number of creditors is limited, settlement may offer a practical solution.

Working with a debt settlement lawyer ensures negotiations are handled professionally and legally. An attorney can review account histories, identify defenses if litigation has begun, and negotiate terms that protect your financial interests while minimizing long-term consequences.

When Debt Relief Is Not Enough

While debt settlement and negotiation can be effective tools, there are situations where these options may not fully resolve the problem. One clear sign is when multiple creditors have already filed lawsuits. Defending several cases at once can become expensive and time-sensitive, especially if judgments are entered.

Another serious warning sign is the threat of foreclosure. In Texas, most home foreclosures proceed without a lawsuit because the state allows non-judicial foreclosure for regular purchase-money mortgages. If you are behind on payments and facing a scheduled sale date, settlement of unsecured debts alone may not address the immediate risk to your home.

Persistent collection pressure is also an indicator that informal negotiations may not be sufficient. If creditors refuse to settle, continue aggressive collection efforts, or escalate matters to court, a more structured legal solution may be necessary to stop debt collectors from advancing their claims.

Accumulating secured debt, such as mortgage arrears or vehicle loan defaults, can further complicate the situation. Unlike unsecured debt, secured obligations are tied to property, meaning creditors have the right to repossess or foreclose if payments remain unpaid.

In these circumstances, consulting a debt relief attorney is critical. Bankruptcy may be a better approach if alternatives fail, particularly when multiple legal actions, secured debt issues, or significant financial hardship make settlement unrealistic. A thorough legal review can determine whether restructuring debt through Chapter 7 or Chapter 13 offers stronger and more comprehensive protection.

Bankruptcy as a Structured Debt Relief Option

Chapter 7 Bankruptcy

When other debt relief options are no longer realistic, bankruptcy provides a structured and court-supervised solution. Chapter 7 bankruptcy is often referred to as a liquidation bankruptcy. Still, for many individuals in Texas, it primarily serves as a way to eliminate overwhelming unsecured debt while protecting exempt property.

Eligibility for Chapter 7 is determined by a means test, which compares your income to the median income for a household of your size in Texas. If your income falls below the threshold, you may qualify automatically. If it exceeds the limit, additional calculations are required to determine whether disposable income is sufficient to repay creditors. Qualification depends on accurate financial disclosure, including income, expenses, and total debt obligations.

One of the primary benefits of Chapter 7 is the discharge of unsecured debts. This may include credit card balances, medical bills, personal loans, and certain collection accounts. Once discharged, these debts are legally eliminated, and creditors are prohibited from attempting further collection. This relief can provide a meaningful financial reset for individuals who have no realistic ability to repay what they owe.

Texas law provides strong asset exemptions that often allow filers to retain essential property. The Texas homestead exemption can protect a primary residence in many situations, subject to federal limitations. Personal property exemptions may also apply to vehicles, household goods, and certain retirement accounts. Proper planning and accurate filings are critical to ensuring assets remain protected.

Working with an experienced Chapter 7 bankruptcy attorney ensures that all required documents are properly prepared and filed with the court. A knowledgeable attorney can evaluate eligibility, explain how exemptions apply to your specific situation, and guide you through the process in the Southern District of Texas. With careful legal guidance, Chapter 7 can offer a lawful and effective path toward financial stability.

Chapter 13 Bankruptcy

Chapter 13 bankruptcy is designed for individuals who have regular income but need time to reorganize their debts. Instead of eliminating debts immediately like Chapter 7, Chapter 13 creates a structured repayment plan lasting three to five years. During this period, you make monthly payments to a trustee, who distributes funds to creditors according to a court-approved plan.

Chapter 13 is often appropriate for individuals who are behind on secured debts, particularly mortgages or vehicle loans, but want to keep their property. One of its primary benefits is the ability to catch up on mortgage arrears over time while continuing regular monthly payments. This structure can prevent foreclosure if payments are maintained under the plan.

There are eligibility limits for Chapter 13. Currently, unsecured debts must not exceed $526,700, and secured debts must not exceed $1,580,125. These limits apply at the time of filing and are important when determining whether Chapter 13 is available as an option.

A knowledgeable Chapter 13 bankruptcy attorney plays a critical role in preparing accurate repayment plans, calculating disposable income, and ensuring compliance with court requirements. Proper planning can make the difference between a confirmed plan and dismissal of the case.

How Bankruptcy Protects Against Foreclosure

In Texas, most home foreclosures do not require a lawsuit because the state allows non-judicial foreclosure for standard purchase-money mortgages. This means a lender may proceed with foreclosure without filing a court case, provided required notices are given. However, certain situations—such as home equity loans, reverse mortgages, and property tax lien transfers—do require judicial approval.

When you file for bankruptcy, an automatic stay goes into effect immediately. This court order temporarily halts foreclosure proceedings, collection efforts, and most creditor actions. For homeowners facing a scheduled sale date, this protection can provide crucial time to reorganize finances or propose a Chapter 13 repayment plan.

For individuals considering whether to file for bankruptcy relief, understanding how the automatic stay works is essential. Bankruptcy does not eliminate a mortgage automatically, but it can create a structured opportunity to protect your home under federal law.

Working with a Bankruptcy Lawyer

Bankruptcy requires precise documentation, strict adherence to deadlines, and full financial disclosure. Errors or omissions can delay proceedings or jeopardize protections. Working with an experienced bankruptcy attorney ensures that petitions, schedules, and repayment plans are properly prepared and filed in the Southern District of Texas.

Joel Gonzalez practices in the Southern District, serving clients in Corpus Christi, Houston, Victoria, McAllen, Laredo, and surrounding communities. As an individual bankruptcy lawyer, he works directly with clients to evaluate eligibility, apply Texas exemptions correctly, and guide cases through the court process.

Choosing a qualified bankruptcy lawyer can help ensure that your case is handled carefully, your rights are protected, and your debt relief strategy aligns with your long-term financial goals.

How to Evaluate Which Debt Relief Option Is Right for You

Choosing the right debt relief strategy begins with an honest assessment of your financial situation. Start by separating unsecured debt, such as credit cards and medical bills—from secured debt like mortgages and vehicle loans. The type and amount of debt you carry will heavily influence whether settlement, structured repayment, or bankruptcy makes sense.

You should also ask whether you are currently facing lawsuits. If creditors have already filed cases, defending those actions may require a different strategy than simple negotiation. Likewise, if foreclosure is pending, timing becomes critical. In Texas, where many foreclosures proceed without court involvement, delays can quickly limit your available options.

Income stability is another key factor. If you have consistent earnings, structured repayment through settlement or Chapter 13 bankruptcy may be realistic. If income is uncertain or insufficient to meet basic obligations, Chapter 7 may provide more meaningful relief.

When comparing settlement versus bankruptcy, consider both immediate relief and long-term consequences. Settlement may reduce balances, but it does not provide automatic legal protection from all creditors. Bankruptcy offers court-supervised protection but has a more significant impact on credit reporting. Negotiation can work in early stages, while court defense may be necessary once a lawsuit has been filed.

Be cautious of unrealistic guarantees or promises that sound too good to be true. Every financial situation is different. Consulting a debt relief law firm allows you to receive a clear legal evaluation based on Texas law and your specific circumstances, rather than relying on generalized advice or marketing claims.

Texas-Specific Considerations

Texas offers some of the most debtor-friendly property exemptions in the country. Under Texas law, certain assets may be protected from creditors, including personal property up to statutory limits and qualified retirement accounts. Most notably, Texas provides strong homestead protections, often allowing homeowners to exempt the full value of their primary residence (subject to acreage limitations), which can be especially important when evaluating bankruptcy or responding to a foreclosure lawsuit homeowners may be facing.

Understanding how these exemptions apply requires careful legal analysis. While federal bankruptcy exemptions exist, Texas residents typically choose state exemptions because they are more generous in many cases. The right exemption strategy can determine whether property is retained or liquidated in a Chapter 7 filing.

For residents filing in the Southern District of Texas, local procedural rules and trustee expectations matter. This district includes divisions in Houston, Victoria, Corpus Christi, McAllen, and Laredo. Each division may have specific administrative practices, hearing procedures, and judicial preferences that influence case outcomes.

Working with experienced bankruptcy lawyers ensures familiarity with both statewide exemption laws and the procedural nuances of the Southern District. Local knowledge can streamline filings, prevent costly mistakes, and improve the likelihood of a successful outcome.

Common Mistakes When Seeking Debt Relief

One of the most common mistakes people make is waiting too long to seek help. Financial problems rarely resolve on their own. As balances grow, late fees accumulate, and interest compounds, options may become more limited and more expensive. Acting early often preserves more choices.

Ignoring lawsuits is another serious error. Once a creditor files suit, deadlines apply. Failing to respond can result in a default judgment, wage garnishment (where applicable), or frozen bank accounts. Even if you intend to negotiate, you must address court proceedings promptly to protect your rights.

Many individuals also turn to non-legal debt settlement companies without fully understanding the risks. These companies may charge substantial fees and cannot provide legal representation if a creditor sues. In contrast, working with a licensed attorney ensures you receive advice tailored to your specific legal situation.

Another frequent oversight is failing to review eligibility for bankruptcy. Some people assume they will not qualify without ever completing a proper means test analysis. Others misunderstand debt limits for Chapter 13 bankruptcy and dismiss it prematurely. A detailed financial review can clarify which options are actually available under Texas and federal law.

Regain Control: Make Informed Choices for Debt Relief

If you are facing mounting unsecured debt, lawsuits, or foreclosure pressure, early legal advice can make a significant difference. Waiting often reduces flexibility and increases financial stress. A qualified bankruptcy lawyer residents trust can evaluate your income, assets, and debt structure to determine the most strategic path forward.

Joel Gonzalez, a bankruptcy lawyer, helps individuals throughout the Southern District of Texas, including Houston, Victoria, Corpus Christi, McAllen, Laredo, and surrounding communities. As an individual attorney, not a large firm, he works directly with clients to evaluate whether negotiation, settlement, or bankruptcy is the right path forward.

To explore your options and receive guidance tailored to your situation, visit The Law Office of Joel Gonzalez.