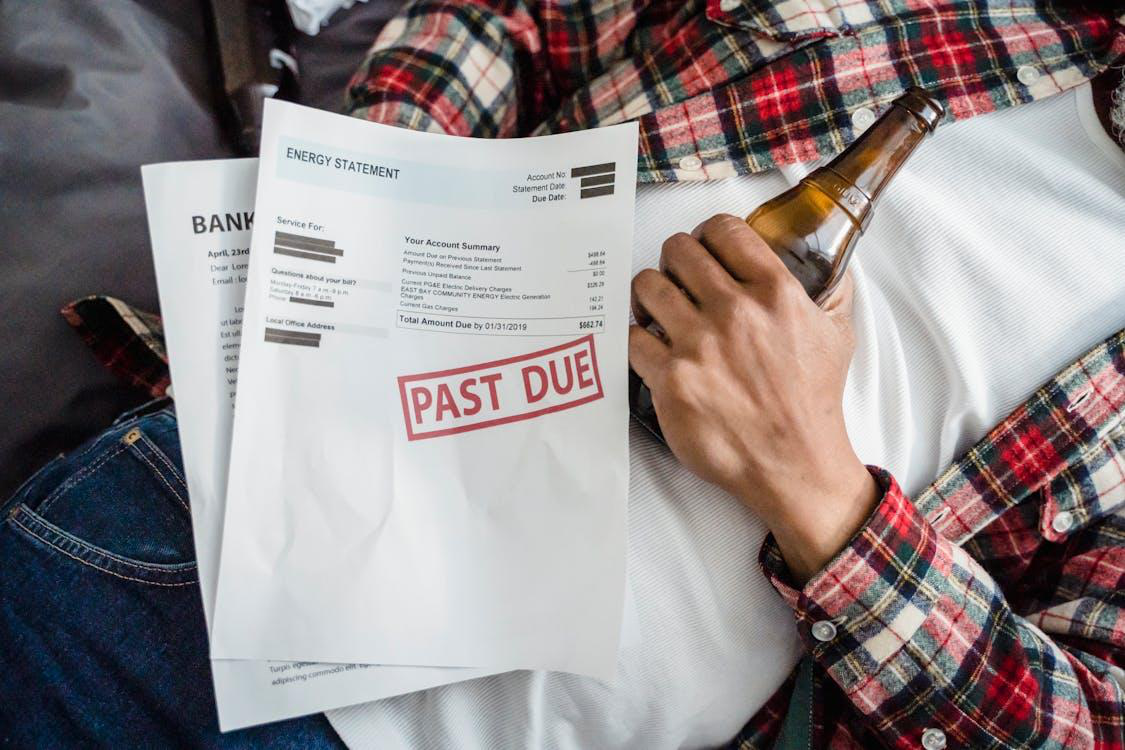

Rising housing costs, medical bills, reduced work hours, and other financial setbacks can make it harder to stay current on a mortgage. When that pressure builds, understanding foreclosure risks becomes an important first step. Missing payments does not always mean a home will be lost right away, but delays can narrow the options available. In Texas, many standard mortgage foreclosures move through a non-judicial process, which means a lender may not need to file a lawsuit before scheduling a sale.

Know What Can Trigger the Foreclosure Process

Foreclosure usually begins after missed mortgage payments, but payment default is not the only issue that can create serious trouble. Loan terms may also require homeowners to maintain insurance, pay property taxes, and respond to notices from the servicer. Falling behind in any of these areas can increase the risk of acceleration and a pending sale date. For some borrowers, the best first step is reviewing the loan documents and speaking with a bankruptcy lawyer about how different forms of debt pressure may be affecting the household budget.

Understand When Court Involvement May or May Not Happen

Many homeowners assume every foreclosure leads to a courtroom battle, but that is not always how the process works in Texas. For many traditional purchase-money mortgages, lenders may use the non-judicial process if the deed of trust allows it and required notices are sent properly. However, some matters can involve court action, including certain home equity loans, tax lien issues, or disputes over whether foreclosure procedures were followed correctly. In those situations, guidance from a foreclosure lawsuit attorney may be valuable if there are questions about notice, timing, loan type, or available defenses.

Consider Whether Bankruptcy May Be a Better Path Forward

When mortgage delinquency is tied to larger debt problems, a broader legal solution may deserve serious review. In some situations, it may provide time to catch up on arrears through a repayment plan or discharge certain unsecured obligations that are draining income. A consultation with a bankruptcy attorney can help determine whether bankruptcy may be a better approach when a modification or negotiated workout is not realistic.

Take Action Before Fewer Options Remain

If you are worried about losing your home, waiting for the problem to resolve itself can make the situation harder to fix. At Joel Gonzalez, we work directly with individuals and families who need straightforward guidance on foreclosure concerns, debt pressure, and bankruptcy-related decisions.

Whether you are trying to understand notices from a lender, compare alternatives, or speak with a debt relief attorney in Rockport, TX, we can help you evaluate practical next steps with clarity and care. If bankruptcy may be the better path, we can also discuss how a bankruptcy lawyer in Aransas, TX may help protect your interests. To discuss your specific needs and explore how we can help, reach out today.