A lawsuit notice arrives unexpectedly. The envelope is opened, and a sinking feeling follows. Questions start racing through a person’s mind. What happens next? Will property be taken? Is foreclosure inevitable? Can creditors keep filing lawsuits? Is there any realistic path toward relief?

These concerns affect many Americans every year. Millions of debt collection cases are filed annually across the United States, placing significant pressure on individuals and families struggling with financial obligations.

When debt problems extend beyond a single creditor and begin involving collection lawsuits, foreclosure threats, vehicle repossession notices, and mounting unsecured debt, the situation can feel impossible to manage without legal guidance.

This is where a bankruptcy lawyer often becomes an important part of the solution. Rather than addressing one problem at a time, bankruptcy law offers tools that can address multiple financial challenges simultaneously. Whether someone needs a Chapter 7 bankruptcy attorney to eliminate qualifying debts or a Chapter 13 bankruptcy attorney to create a structured repayment plan, legal options may provide a path toward lasting relief.

For those facing mounting debt pressure, the Law Office of Joel Gonzalez provides focused bankruptcy guidance aimed at helping individuals move from creditor action toward workable financial relief.

This article follows the story of a typical debtor from the moment a lawsuit is received through the final resolution of multiple financial problems, showing how a bankruptcy attorney in Corpus Christi may help coordinate legal protections across several fronts at once.

Meet the Typical Client: When Debt Problems Begin to Multiply

Consider a hypothetical client named Michael.

For years, Michael managed his finances responsibly. He worked steadily, paid bills on time, and maintained reasonable credit. Then several setbacks occurred within a relatively short period.

- Unexpected medical expenses appeared.

- Credit card balances increased.

- Interest charges grew.

- A reduction in household income created additional strain.

At first, Michael believed he could recover on his own. He made minimum payments and tried to negotiate with creditors. Unfortunately, the balances continued growing faster than he could reduce them.

- Soon, collection calls became more frequent.

- Then came the first lawsuit.

Stage One: Receiving the Debt Collection Lawsuit

Many people assume a debt collection lawsuit automatically means they have already lost the case. That is not true.

A lawsuit is simply the beginning of a legal proceeding. However, ignoring it can create serious consequences.

When Michael received notice that a creditor had filed suit against him, he faced several immediate concerns:

- Court deadlines

- Required responses

- Potential judgments

- Additional legal fees

- Ongoing collection activity

The lawsuit itself was stressful enough. Yet it represented only one part of a larger financial problem.

Michael also had:

- Significant credit card debt

- Medical bills

- Personal loan obligations

- Mortgage arrears

- Vehicle payment issues

Addressing only the lawsuit would not solve the broader financial difficulties.

This is often the point where individuals begin speaking with bankruptcy lawyers to evaluate all available options.

Looking Beyond the Lawsuit

A debt lawsuit can create urgency, but effective legal planning usually requires looking at the complete financial picture.

Before deciding how to proceed, several factors typically need review:

Existing Debts

A complete list of obligations helps determine whether bankruptcy relief may be appropriate.

This often includes:

- Credit cards

- Medical debt

- Personal loans

- Collection accounts

- Deficiency balances

- Certain judgment debts

Property Ownership

Assets may influence whether Chapter 7 or Chapter 13 provides the better solution.

Examples include:

- Homes

- Vehicles

- Savings accounts

- Business interests

- Investment property

Income and Expenses

Current financial circumstances help determine eligibility for various bankruptcy options.

Pending Legal Actions

Many debtors face more than one legal threat at a time.

Some have:

- Collection lawsuits

- Foreclosure proceedings

- Repossession risks

- Tax-related issues

- Multiple creditor actions

Reviewing all these matters together creates a clearer path forward.

Stage Two: The Threat of a Court Judgment

As Michael’s lawsuit progressed, another concern emerged.

If the creditor obtained a judgment, collection efforts could become more aggressive.

Many consumers focus entirely on defending the lawsuit itself. However, even a successful defense may not solve broader debt issues if multiple creditors are involved.

Michael realized that eliminating one lawsuit would still leave him with:

- Several other delinquent accounts

- Mortgage payment problems

- Vehicle payment concerns

- Growing interest charges

At this point, the question shifted from “How do I stop this lawsuit?” to “How do I solve the entire debt problem?”

That distinction often changes everything.

Understanding the Bigger Financial Picture

When debts become interconnected, separate solutions may create additional complications.

For example:

- A homeowner may attempt to settle a credit card lawsuit while simultaneously falling behind on mortgage payments.

- A vehicle owner may focus on repossession prevention while medical debtscontinue growing.

- A consumer may negotiate with one creditor only to face lawsuits from several others months later.

- Addressing issues one by one can become expensive and time-consuming.

Bankruptcy law offers a framework designed to handle multiple debt-related problems within a single legal process.

Stage Three: Foreclosure Notices Enter the Story

Several months after receiving the lawsuit, Michael faced another challenge.

- He had fallen behind on mortgage payments.

- A foreclosure notice arrived.

- The situation now involved more than unsecured debt. His home was potentially at risk.

Many people do not realize that debt lawsuits and foreclosure actions frequently occur at the same time.

When income becomes strained, difficult choices often follow:

- Pay the mortgage or the credit cards?

- Pay medical bills or vehicle payments?

- Catch up on one debt or spread funds among many creditors?

Eventually, somebody remains unpaid.

When mortgage arrears continue growing, foreclosure becomes a possibility.

For Michael, the debt lawsuit that once seemed like the primary problem suddenly became only one piece of a larger financial crisis.

Why Timing Matters

- Waiting too long can limit available options.

- Once foreclosure proceedings begin, deadlines become increasingly important.

- Taking action earlier often provides more flexibility.

- That does not necessarily mean bankruptcy is always the right answer.

However, evaluating bankruptcy options before major legal deadlines pass can provide valuable information.

A bankruptcy lawyer may assess:

- Foreclosure status

- Lawsuit deadlines

- Repossession risks

- Debt amounts

- Income qualifications

- Asset protection concerns

The earlier this review occurs, the more options may be available.

Stage Four: Vehicle Repossession Becomes a Concern

While trying to address the lawsuit and mortgage issues, Michael encountered another setback.

- His vehicle payments fell behind.

- Soon, repossession became a possibility.

- For many households, losing transportation creates immediate hardships.

It can affect:

- Employment

- Medical appointments

- Childcare arrangements

- Daily responsibilities

This illustrates a common pattern.

Financial problems rarely remain isolated.

One missed payment can lead to another.

Then another.

Eventually multiple creditors begin pursuing separate remedies at the same time.

At this stage, individuals often need a comprehensive legal solution rather than a series of temporary fixes.

How Bankruptcy Can Affect Multiple Legal Problems Simultaneously

One reason people consult a bankruptcy lawyer is that bankruptcy law may provide protections that reach across several different creditor actions.

Depending on the circumstances, filing may affect:

- Debt collectionlawsuits

- Collection efforts

- Foreclosure proceedings

- Vehicle repossession actions

- Certain creditor communications

Instead of responding to each creditor separately, a single filing may change how creditors proceed moving forward.

For someone like Michael, this shift can provide an opportunity to organize finances and evaluate long-term solutions.

Stage Five: Evaluating Chapter 7 Bankruptcy

After reviewing his situation, Michael considered whether Chapter 7 might be appropriate.

Chapter 7 is often discussed when a person lacks sufficient income to repay significant unsecured debt.

Many consumers seek guidance from a Chapter 7 bankruptcy attorney when dealing with:

- Credit card balances

- Medical debt

- Personal loans

- Collection accounts

A Chapter 7 case may eliminate qualifying debts and provide a fresh start for certain filers.

However, eligibility requirements apply.

- Not everyone qualifies.

- Additionally, every case involves a careful review of assets, income, exemptions, and financial history.

- For some individuals, Chapter 7provides the most direct route toward debt relief.

- For others, Chapter 13 may offer greater benefits.

Stage Six: When Chapter 13 May Be the Better Option

- Michael’s mortgage situation complicated matters.

- He wanted to keep his home.

- He also needed time to address mortgage arrears.

- As a result, Chapter 13became an important option to consider.

A Chapter 13 bankruptcy attorney typically evaluates whether a structured repayment plan could help address specific financial goals.

Chapter 13 may be particularly useful when someone needs time to:

- Catch up on mortgage arrears

- Address vehicle payment issues

- Reorganize debt obligations

- Manage multiple creditor claims

Instead of focusing solely on debt elimination, Chapter 13 creates a court-approved repayment framework for qualifying debts.

For many homeowners, this can be an important tool when foreclosure concerns exist.

Comparing Immediate Relief With Long-Term Goals

One of the most significant parts of the legal process involves determining which option best aligns with a person’s objectives.

Questions often include:

Is Keeping the Home the Primary Goal?

If so, strategies may differ significantly from cases focused solely on debt discharge.

Is Vehicle Retention Important?

Transportation concerns often influence legal planning.

How Much Debt Exists?

Debt structure matters just as much as total debt amount.

What Is the Income Situation?

Current and anticipated income may affect available options.

A bankruptcy attorney evaluates these factors together rather than viewing them separately.

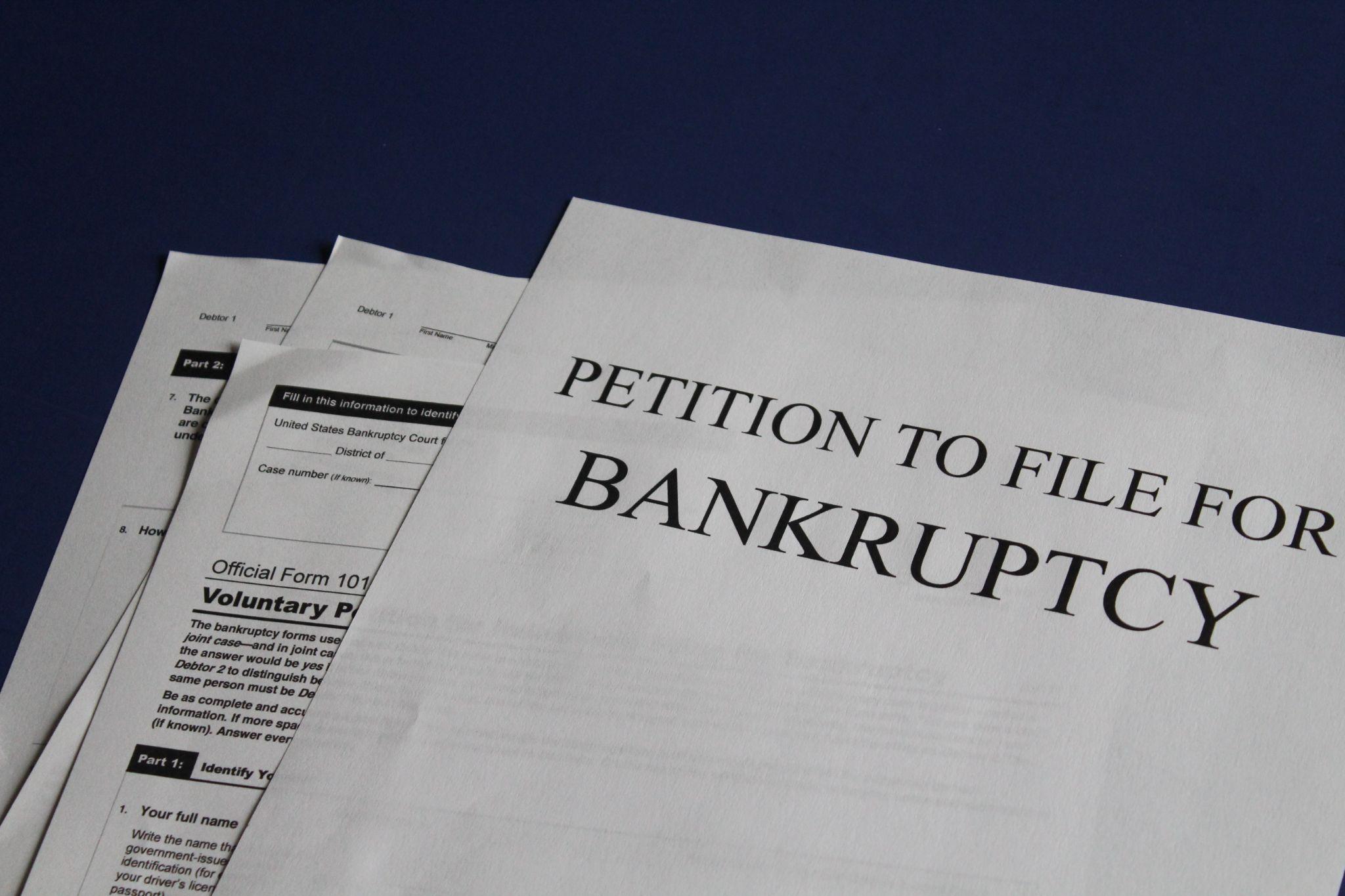

Stage Seven: Filing for Bankruptcy Relief in Texas

After reviewing his circumstances, Michael decided to file for bankruptcy relief in Texas.

- The filing represented a turning point.

- For months, financial pressure had been increasing.

- The lawsuit was pending.

- Foreclosure concerns existed.

- Repossession risks remained.

- Now there was a formal legal process in place to address those issues.

Many clients describe this stage as the first time they feel a sense of direction after months or years of financial uncertainty.

The filing itself requires careful preparation.

Documentation often includes:

- Income information

- Expense information

- Asset disclosures

- Debt schedules

- Creditor information

- Financial records

Accuracy is important throughout the process.

What Happens After Filing?

- Many people assume filing bankruptcy immediately ends the process.

- In reality, filing begins a structured legal proceeding.

- Following filing, several steps typically occur.

Creditor Notification

Creditors receive notice of the case.

Court Procedures

Required bankruptcy procedures continue according to applicable rules.

Financial Review

The court and trustee review submitted information.

Additional Documentation

Certain supporting materials may be requested.

Each case follows its own timeline depending on the chapter filed and the individual’s circumstances.

Coordinating Multiple Legal Matters at Once

One of the most valuable aspects of bankruptcy law is its ability to address interconnected financial problems.

Returning to Michael’s situation:

Before filing, he faced:

- A debt collectionlawsuit

- Mortgage delinquency

- Potential foreclosure

- Vehicle payment problems

- Multiple unsecured debts

Each issue had separate deadlines.

Each creditor had separate objectives.

Each problem required attention.

After entering the bankruptcy process, those matters could be evaluated within a single legal framework.

This often creates greater efficiency than fighting multiple legal battles independently.

When a Single Legal Strategy Makes More Sense Than Multiple Battles

What if the lawsuit sitting on the kitchen table is only one symptom of a much larger debt problem?

For many consumers, that is exactly the situation they face. Collection lawsuits, foreclosure threats, mounting unsecured debt, and repossession concerns often arrive together, creating a cycle that becomes increasingly difficult to manage without legal guidance. Rather than fighting separate battles with each creditor, a comprehensive strategy may provide a more effective path toward relief.

For individuals considering their options, the Law Office of Joel Gonzalez provides experienced guidance from a bankruptcy lawyer in Corpus Christi who understands how debt lawsuits, foreclosure proceedings, and other financial pressures often intersect.

Whether someone may benefit from working with a Chapter 7 bankruptcy attorney or a Chapter 13 bankruptcy attorney, the goal is to identify practical solutions based on the client’s unique circumstances.

Those seeking to file for bankruptcy relief in Texas can contact the Law Office of Joel Gonzalez to discuss available options and learn how an experienced bankruptcy attorney in Corpus Christi can help move a case from crisis toward resolution.