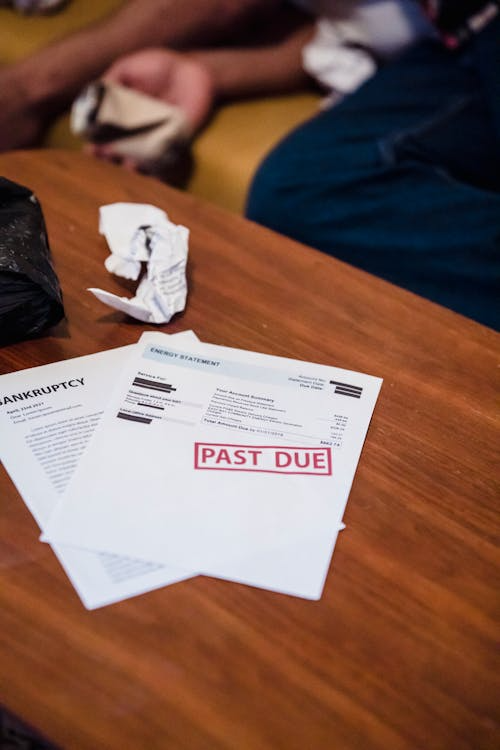

Consumer debt levels in the United States remain historically high, with Federal Reserve data showing household debt exceeding $18.8 trillion in recent years. For many South Texas families, rising interest rates and unexpected expenses have made repayment increasingly difficult. When financial strain becomes unmanageable, residents often face a critical decision: Debt Settlement vs. Bankruptcy. Understanding how each option works—and which may save more money based on income and total debt—is essential before taking action.

A qualified debt settlement lawyer frequently evaluates both paths for clients, comparing legal protections, repayment obligations, and long-term financial outcomes.

How Debt Settlement Works

Debt settlement involves negotiating directly with creditors to reduce the total balance owed. This process is typically handled by a debt relief law firm in Beeville.

In most cases:

- Creditors agree to accept a lump-sum payment that is less than the full balance.

- Accounts may be reported as “settled” rather than “paid in full.”

- There is no automatic court protection from lawsuits.

Debt settlement may be appropriate for individuals with steady income who can accumulate funds for negotiated payments.

However, it does not automatically stop a foreclosure lawsuit or prevent vehicle repossession. In those situations, consulting a repossession lawyer in Beeville may be necessary.

How Bankruptcy Provides Legal Protection

Bankruptcy is a federal legal process that can discharge or restructure debts under court supervision. Filing triggers an automatic stay, which immediately halts collection actions, including lawsuits and certain garnishments.

Bankruptcy may also provide relief from tax levies in Beeville, depending on eligibility and the nature of the debt.

Unlike debt settlement, bankruptcy provides:

- Court-enforced protection from creditors

- Structured repayment plans under Chapter 13

- Potential discharge of unsecured debts under Chapter 7

For some households, bankruptcy may ultimately reduce total repayment amounts more significantly than settlement, particularly when income limitations qualify them for discharge.

Comparing Financial Outcomes for Beeville Residents

When evaluating Debt Settlement vs. Bankruptcy, several factors determine which path saves more money:

- Total unsecured debt

- Monthly income and expenses

- Risk of pending lawsuits

- Exposure to repossession or foreclosure

A debt relief law firm can conduct a financial analysis to estimate long-term costs under each option.

Settlement may work for moderate debt with stable earnings. Bankruptcy may offer stronger protection when debt exceeds repayment capacity.

Making an Informed Financial Decision

Choosing between Debt Settlement vs. Bankruptcy requires careful legal and financial evaluation. Each option carries distinct implications for credit, asset protection, and total repayment.

If you are facing mounting debt, lawsuits, or collection pressure, consult The Law Office of Joel Gonzalez today. A professional assessment can help you determine which solution aligns with your financial circumstances and long-term stability. Contact now!